Federal Employee Retirement System (FERS)

Congress created the Federal Employees Retirement System (FERS) in 1986, and it became effective on January 1, 1987. Since that time, new Federal civilian employees who have retirement coverage are covered by FERS.

FERS is a retirement plan that provides benefits from three different sources: a Basic Benefit Plan, Social Security and the Thrift Savings Plan (TSP). Two of the three parts of FERS (Social Security and the TSP) can go with you to your next job if you leave the Federal Government before retirement. The Basic Benefit and Social Security parts of FERS require you to pay your share each pay period. Your agency withholds the cost of the Basic Benefit and Social Security from your pay as payroll deductions. Your agency pays its part too. Then, after you retire, you receive annuity payments each month for the rest of your life.

The TSP part of FERS is an account that your agency automatically sets up for you. Each pay period your agency deposits into your account amount equal to 1% of the basic pay you earn for the pay period. You can also make your own contributions to your TSP account and your agency will also make a matching contribution. These contributions are tax-deferred. The Thrift Savings Plan is administered by the Federal Retirement Thrift Investment Board.

For more information about TSP, see their website (external link). See the SSA website (external link) for more information about the Social Security portion of your retirement benefit. This website covers the Federal Employees Retirement System. Through the menu links on the left, you can find information about the following FERS retirement topics:

FERS is a retirement plan that provides benefits from three different sources: a Basic Benefit Plan, Social Security and the Thrift Savings Plan (TSP). Two of the three parts of FERS (Social Security and the TSP) can go with you to your next job if you leave the Federal Government before retirement. The Basic Benefit and Social Security parts of FERS require you to pay your share each pay period. Your agency withholds the cost of the Basic Benefit and Social Security from your pay as payroll deductions. Your agency pays its part too. Then, after you retire, you receive annuity payments each month for the rest of your life.

The TSP part of FERS is an account that your agency automatically sets up for you. Each pay period your agency deposits into your account amount equal to 1% of the basic pay you earn for the pay period. You can also make your own contributions to your TSP account and your agency will also make a matching contribution. These contributions are tax-deferred. The Thrift Savings Plan is administered by the Federal Retirement Thrift Investment Board.

For more information about TSP, see their website (external link). See the SSA website (external link) for more information about the Social Security portion of your retirement benefit. This website covers the Federal Employees Retirement System. Through the menu links on the left, you can find information about the following FERS retirement topics:

- Eligibility – The main eligibility requirements for the common types of retirements.

- Computation – How your retirement annuity is computed.

- Creditable Service – Rules showing the civilian and military service that can be used to compute your FERS retirement benefits.

- Planning and Applying – It's never too early to start planning for retirement in order to ensure it goes smoothly. Here you will find information to help ensure your retirement starts well.

- Early Retirement – Explanation of the minimum retirement age and early retirement if your agency under goes a “reduction in force” or you are involuntarily separated other than for cause.

- Types of Retirement – Learn about the age, service requirements and considerations affecting the various types of retirement.

- Deferred – If you are a former Federal employee who was covered by the Federal Employees Retirement System (FERS), you may be eligible for a deferred annuity at age 62 or the Minimum Retirement Age (MRA).

- Survivors – When a Federal employee dies, monthly or lump sum benefits may be payable to survivors. Learn about these Survivor benefits here.

- Military Retired Pay – Adding military service to your civilian service

- Service Credit – Payment to increase your annuity for civilian service when no CSRS retirement deductions were withheld or were refunded or for military service after 1956.

- Former Employees – Options if you leave your Government job before becoming eligible for retirement.

|

Eligibility is determined by your age and number of years of creditable service. In some cases, you must have reached the Minimum Retirement Age (MRA) to receive retirement benefits. Use the following chart to figure your Minimum Retirement Age.

MORE... |

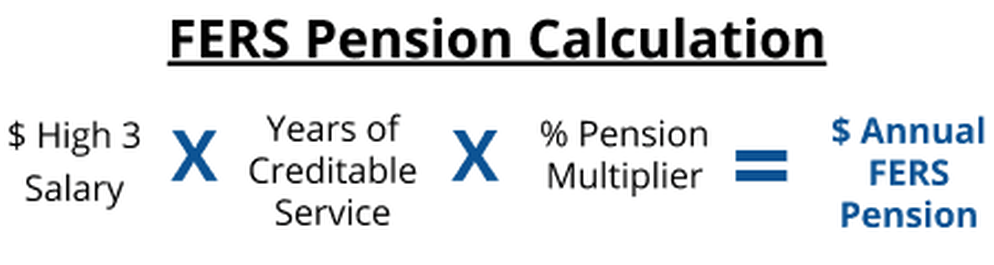

Your basic annuity is computed based on your length of service and “high-3” average salary. To determine your length of service for computation, add all your periods of creditable service, then eliminate any fractional part of a month from the total.

High-3 Average Salary

Your “high-3” average pay is the highest average basic pay you earned during any 3 consecutive years of service. These three years are usually your final three years of service, but can be an earlier period, if your basic pay was higher during that period.

Computation for Non-Disability Retirements

FERS Basic Annuity Formula

High-3 Average Salary

Your “high-3” average pay is the highest average basic pay you earned during any 3 consecutive years of service. These three years are usually your final three years of service, but can be an earlier period, if your basic pay was higher during that period.

Computation for Non-Disability Retirements

FERS Basic Annuity Formula

|

|

Your benefit was computed differently, if you retired under one of the provisions below

|

Special Provision for Air Traffic Controllers, Firefighters, Law Enforcement Officers, Capitol Police, Supreme Court Police, or Nuclear Materials Couriers

|

Member of Congress or Congressional Employee (or any combination of the two) must have at least 5 years of service as a Member of Congress and/or Congressional Employee

|

Federal Employee Benefit Planners LLC, and Birdseye Financial INC, and the website contents are not affiliated nor owned by any U.S. government agency or affiliate. The information provided on www.federalbenefitsnow.com and www.birdseyefinancial is for informational purposes only and is not intended to be a source of advice or credit analysis with respect to the material presented. The information and/or documents contained on this website do not constitute legal or financial advice and should never be used without first consulting with an insurance and/or a financial professional to determine what may be best for your individual needs. Federal Employee Benefit Planners LLC, Birdseye Financial, the publisher and the author of this website do not make any guarantee or other promise as to any results that may be obtained through the information and services offered. You should never make any investment decision without first consulting with your own financial advisor and conducting your own research and due diligence. To the maximum extent permitted by law, the publisher and the author disclaim any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations contained in this book prove to be inaccurate, incomplete or unreliable, or result in any investment or other losses. Although the author and publisher have made every effort to ensure that the information found on this website are correct at press time, the author and publisher do not assume and hereby disclaim any liability to any party for any loss, damage, or disruption caused by errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause. Content contained or made available through this website do not intended to and does not constitute legal advice or investment advice and no attorney-client relationship is formed. The publisher and the author are providing the website and its contents on an “as is” basis. Your use of the information on this website is at your own risk.